When you're hiring someone to work on your home, you'll hear the terms "bonded" and "insured" thrown around a lot. They sound similar, but they protect you from completely different problems. The easiest way to think about it is this: insurance protects against accidents, while a bond protects you from theft or shoddy work.

One is about honest mistakes, the other is about a company's integrity. It's a critical distinction to understand before letting any contractor start a job at your Phoenix-area home.

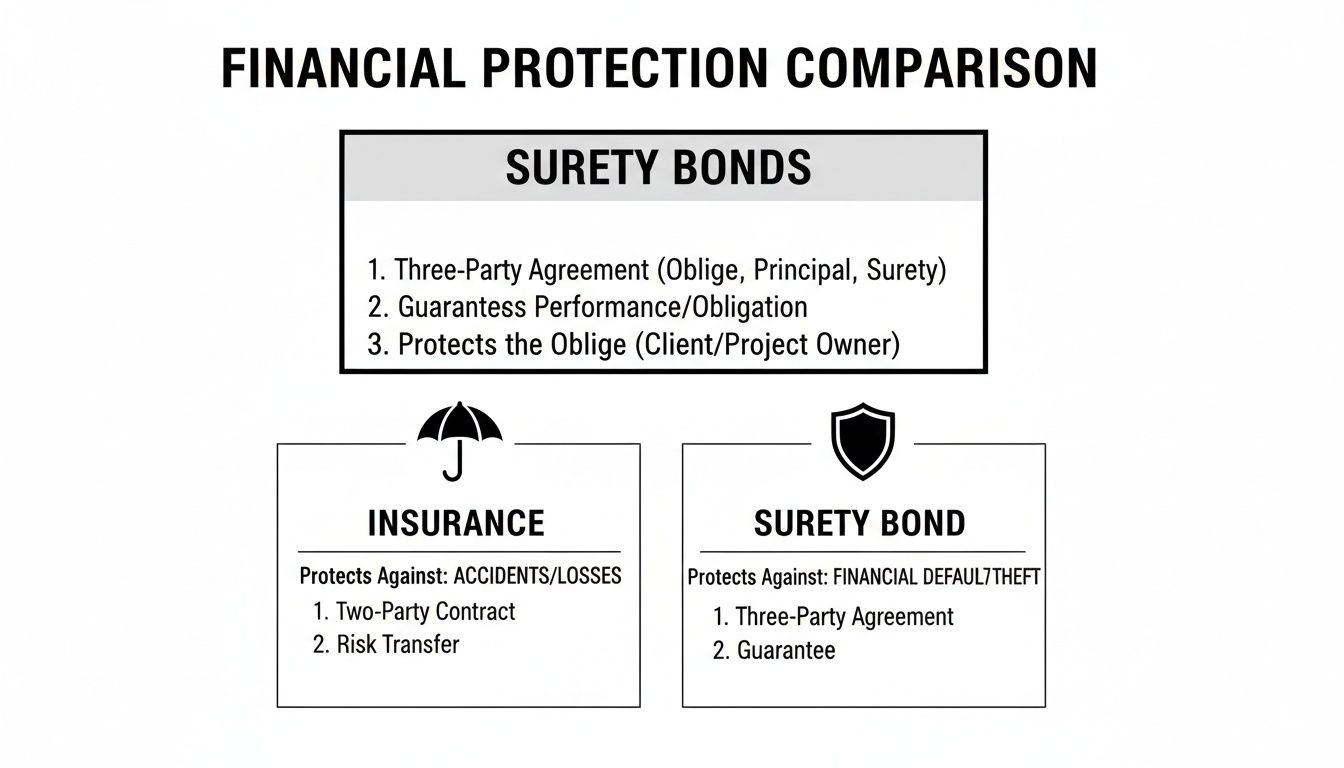

Understanding the Core Protections for Your Home

Inviting a window cleaning crew or any service professional to your property means you're placing a huge amount of trust in them. The phrases "bonded and insured" aren't just marketing fluff; they represent two distinct layers of financial security that cover very different kinds of risks. Any truly professional company will have both in place, and you shouldn't settle for less.

Think of it this way: insurance handles the "oops" moments, while a bond deals with deliberate wrongdoing or a contractor who simply doesn't finish the job.

What Being Insured Means

When a contractor says they're insured, they're talking about carrying an insurance policy—usually general liability insurance. This is their safety net for the unexpected accidents that can happen on a job site.

If a technician is cleaning a high window and accidentally drops a squeegee that cracks your expensive tile below, their insurance policy is what pays for the repair. If someone slips on a wet spot and gets hurt, the policy covers those medical costs. It protects their business from financial disaster, but more importantly, it ensures you're not left holding the bill for their mistake.

What Being Bonded Means

Being bonded is a completely different animal. A bond is essentially a financial guarantee purchased by the contractor from a third-party company (a surety company). This bond is there to protect you, the client.

If an employee of the company steals something from your home, or if the business takes your deposit and never shows up to do the work, you can file a claim against their bond to get your money back. It's a specific safeguard against theft, fraud, or a contractor failing to live up to their end of the deal.

The cost difference between these two protections really tells the story. For a window cleaning business, a general liability policy might cost around $719 annually, while a surety bond could be as low as $126 per year. This shows how each one is designed to cover a very different type of risk, which is why having both is so important. For a closer look at industry specifics, you can check out a detailed window cleaning industry analysis.

A simple way to remember it: Insurance covers accidents, while a bond covers integrity. One protects against clumsiness, the other against a lack of character.

Bonded vs Insured At a Glance

Sometimes seeing it side-by-side makes the difference click. This quick table breaks down what each type of protection does, what it's for, and who it's really meant to protect.

| Protection Type | What It Covers | Who It Protects | Primary Purpose |

|---|---|---|---|

| Insurance | Accidental property damage, bodily injuries, professional mistakes. | The business owner from financial loss. | To manage the financial risk of unforeseen accidents during operations. |

| Bonding | Employee theft, fraud, failure to complete a job as contracted. | The client or customer from financial loss. | To guarantee the contractor's ethical conduct and contractual obligations. |

As you can see, they serve very different functions. Insurance is for unexpected mishaps, while a bond is a guarantee of the contractor's promise to you. A reputable company will always carry both.

How Contractor Insurance Protects Your Property

While a bond is there to protect you from things like theft, contractor insurance is your real financial shield against the accidents that can happen during a job. The most important policy to look for is general liability insurance. Think of it as the contractor's "oops" fund, designed to cover the costs if they accidentally damage your property or cause an injury while working at your home.

Without it, a simple mistake could spiral into a messy and expensive legal problem for you. This policy is the first line of defense, protecting both the business and you from the financial consequences of an unexpected mishap.

Coverage for Accidental Property Damage

Even the most careful pros have off days. That’s exactly what general liability insurance is for. If a window cleaner is working on your property and accidentally causes damage, their policy—not your homeowner's insurance—is supposed to cover the cost of repairs or replacement.

Here are a few all-too-common scenarios where this coverage is a lifesaver:

- Window Damage: A squeegee blade catches a piece of debris and puts a deep, unfixable scratch in a custom-tinted window.

- Fixture Mishaps: While setting up, a crew member knocks over a ladder, and it shatters an expensive outdoor light fixture on your Phoenix patio.

- Water Damage: A pressure washer hose bursts, sending water seeping under your sliding glass door and buckling the hardwood floor inside.

If the contractor isn't insured, your only option is to chase them down for the money yourself, which is often a long, frustrating, and fruitless process. Having a valid policy on file means there's a clear path to getting things fixed and paid for.

This is a key difference in the bonded vs insured discussion. Insurance pays for accidental damage caused by the contractor or their employees, ensuring you are financially whole after a mishap.

Protection Against Bodily Injury Claims

Property is one thing, but people are another. General liability also protects you if you, a family member, or a guest is accidentally injured because of the contractor’s work. This coverage is meant to handle medical bills and any potential legal costs, keeping you out of a personal injury claim.

Imagine a window cleaner leaves a bucket of water in a walkway, and you trip over it on your way to the mailbox. Their insurance should cover your medical costs. This prevents you from having to file a claim against your own homeowner’s policy, which could jack up your rates for years.

The Role of Workers' Compensation Insurance

It's also crucial to understand the difference between general liability and workers' compensation insurance. General liability covers injuries to you or your guests (non-employees), while workers' comp covers injuries to the contractor’s own employees while they're on your property.

If a technician falls off a ladder and breaks an arm at your Scottsdale home, their employer's workers' comp policy is what pays for their medical treatment and lost wages. This is a massive deal for you as a homeowner. If the company doesn't have it, that injured worker could potentially sue you to cover their expenses, claiming the accident happened on your unsafe property.

Making sure a contractor carries both general liability and workers' compensation creates a complete circle of protection. It ensures that no matter who gets hurt—a guest, you, or one of their crew members—there’s a specific insurance policy ready to handle it. This level of coverage is the true mark of a professional.

What Does It Mean When a Contractor Is "Bonded"?

While insurance acts as a safety net for accidents, a surety bond tackles something entirely different but just as crucial: integrity. When a contractor says they're "bonded," it means a third-party financial institution is backing their promise to operate honestly and fulfill their side of the bargain. It’s a powerful guarantee that protects you from specific types of professional misconduct.

This is the real heart of the "bonded vs. insured" conversation. Insurance is for the "oops" moments—the accidental damage. A bond, on the other hand, is there to protect you from deliberate wrongdoing or a company's failure to meet its obligations. It's a signal that the company you're hiring has been vetted and is financially accountable for its ethical conduct.

Think of a Bond as a Financial Guarantee for Honesty

Picture a bond as a three-way agreement between you (the client), the service provider (the principal), and the surety company. The surety company essentially guarantees the contractor will play by the rules. If the contractor commits a dishonest act—like theft—that causes you a financial loss, the surety company steps in to compensate you up to the bond's limit.

But here's the kicker: this isn't a get-out-of-jail-free card for the contractor. After the surety company pays your claim, they turn right around and collect that same amount from the contractor. This setup creates a powerful incentive for contractors to maintain the highest ethical standards.

A surety bond is basically a vote of confidence in a contractor's integrity, backed by money. It shows they're so sure of their team's trustworthiness that they've paid a financial company to guarantee it.

The Type of Bond That Matters for Home Services

Bonds aren't one-size-fits-all; they're tailored for specific risks. For a homeowner in Scottsdale hiring a window cleaner or maid service, the bond you care about is a janitorial bond (sometimes called a business service bond).

- Janitorial / Business Service Bonds: This bond is designed specifically to protect you from employee theft. If a technician is working in your home and steals jewelry, cash, or electronics, you can file a claim against this bond to be reimbursed. It gives you a straightforward path to getting your money back without a messy legal fight.

You might hear about other types of bonds, but they usually apply to much larger projects.

- Performance Bonds: These are standard in the construction world. A performance bond ensures a contractor finishes a job as agreed. If they walk off the site halfway through building your new patio, the bond provides the funds to hire someone else to complete it. It’s essential for big renovations but overkill for most day-to-day home services.

What a Bond Doesn't Cover

Knowing what a bond won't do is just as important. A janitorial bond has a very narrow focus: protecting you from theft or other intentional, dishonest acts by a company's employees.

A bond will not cover:

- Accidental Damage: A cleaner accidentally knocks over a vase or cracks a window pane? That’s a job for their general liability insurance, not their bond.

- Poor Quality Work: If the windows are streaky or they missed a spot, that's a customer satisfaction issue to take up with the company directly. The bond doesn't apply.

- Injuries: Any injuries, whether to the crew or someone in your home, fall under workers' compensation and general liability insurance policies.

This is the fundamental difference between being bonded and insured. Bonding protects your valuables from theft, while insurance protects your property from accidents. Any truly professional company you invite into your home will have both, giving you complete peace of mind that you're covered no matter what happens.

Bonded vs. Insured: Real-World Scenarios for Peace of Mind

Knowing the textbook definitions of "bonded" and "insured" is one thing, but understanding how they protect you when something actually goes wrong is what truly matters. For homeowners here in Scottsdale, Peoria, and Phoenix, the difference isn't just semantics—it's what stands between a minor inconvenience and a major financial headache.

Let's walk through a few real-life situations to see exactly why hiring a contractor with both types of coverage is so critical.

Scenario 1: The Accidental Shatter

Picture this: a window cleaner is working on the second floor of your home when their squeegee slips from their grasp. It tumbles down and smashes a custom-etched glass panel on your patio door. The replacement quote comes in at a painful $2,500.

This is a classic case of accidental property damage. It wasn't malicious, just an unfortunate slip-up.

- How Insurance Protects You: The contractor’s general liability insurance is built for this exact moment. They file a claim, and their insurance company covers the cost of replacing that expensive glass panel. You're made whole without any hassle.

- Why a Bond Doesn't Apply: A surety bond won't help here. Bonds are about integrity and ethics—they cover things like theft or failure to complete a job, not accidents. Since this was pure clumsiness, the bond isn't relevant.

With an insured contractor, the problem is solved cleanly. If they were uninsured, that $2,500 bill would be yours to deal with, leaving you to chase the contractor in small claims court.

Scenario 2: The Missing Heirloom

Let's shift gears. The crew has just finished cleaning your interior windows. The next day, you notice a valuable earring that was sitting on your nightstand is gone. You have a sinking feeling it was stolen by an employee.

Now we've moved from an accident to an intentional act of dishonesty. This is a breach of trust.

- How a Bond Protects You: This is precisely what a janitorial service bond (a type of surety bond) is for. After filing a police report, you can make a claim against the company's bond. The surety company investigates, and if the theft is substantiated, they reimburse you for the value of the stolen item.

- Why Insurance Doesn't Apply: General liability insurance policies almost universally exclude coverage for intentional criminal acts committed by the company's own employees. It's simply not what the policy is designed to cover.

Without a bond, your only path forward is a difficult and often fruitless lawsuit against the company. A bond gives you a direct financial remedy when an employee's dishonesty costs you.

This chart helps visualize the fundamental difference: insurance is for accidents, while bonds are for theft.

As you can see, insurance acts as your protection from "oops," while a bond protects you from deliberate wrongdoing.

Scenario 3: The On-the-Job Injury

Here's one more scenario. A technician is walking across your freshly washed patio, hits a wet spot, and takes a hard fall, breaking their wrist. They need medical care and can't work for weeks.

This situation involves a worker getting injured on your property, which brings a whole different type of insurance into play.

- How Workers' Compensation Protects You: The contractor's workers' compensation insurance immediately kicks in. It covers the employee's medical bills and lost wages. Most importantly, it prevents them from suing you, the homeowner.

- The Risk of No Coverage: If that company didn't have workers' comp, the injured employee could turn around and sue you for their medical costs, arguing your property was unsafe. This could trigger a claim against your homeowner's policy and send your premiums through the roof.

Think of workers' compensation as a firewall. It protects you from being held financially responsible for injuries that happen to your contractor's team while they're working at your home. It’s absolutely non-negotiable.

Scenario Breakdown: Which Protection Applies?

To make it crystal clear, let's put these common incidents side-by-side to see which policy or bond comes to the rescue. This table shows who pays when things go wrong.

| Incident Scenario | Covered by General Liability Insurance? | Covered by a Surety Bond? | Client's Protection |

|---|---|---|---|

| Technician accidentally breaks your window | Yes | No | The insurance company pays for the damage. |

| An employee is suspected of stealing jewelry | No | Yes | The bonding company reimburses you for the loss. |

| A worker slips and breaks their arm on your patio | No | No | Workers' Comp covers medical bills, protecting you from a lawsuit. |

As you can see, "bonded vs. insured" isn't a choice—it's a combination. Each type of protection covers a unique and serious risk. Having one without the others leaves you exposed.

A truly professional service provider carries all the necessary coverage to protect their clients completely. Before hiring, it’s always a good idea to know what to expect in terms of pricing, which you can learn more about in our window cleaning price guide. Ultimately, hiring a company that is fully bonded and insured is the only way to ensure your total peace of mind.

Questions Every Homeowner Should Ask Their Contractor

Knowing the difference between "bonded" and "insured" is one thing, but actually using that knowledge to vet a contractor is what really protects you. When you’re ready to hire someone for a project at your Phoenix or Scottsdale home, you have to do your homework. Asking the right questions shifts you from a customer into a savvy homeowner who knows exactly what to look for in a pro.

Think of it as having a simple checklist in your back pocket. It helps you cut through the sales pitches and get straight to the facts. Any legitimate, professional company will have the answers ready and won't flinch when you ask for proof.

The Essential Verification Checklist

Before you sign on the dotted line, make these questions a non-negotiable part of the conversation. How a contractor responds tells you a lot about their professionalism.

"Are you both bonded and insured?"

This should be your first question, and the only acceptable answer is a quick, confident "yes." If they stumble, try to explain why they only have one, or worse, tell you it’s not necessary for a job like yours—that's a huge red flag."Can you provide a Certificate of Insurance (COI)?"

Talk is cheap. The COI is the official proof, straight from their insurance provider, detailing what they're covered for and the policy limits. Don’t just take their word for it; ask to see the document."Does your insurance include both general liability and workers' compensation?"

This is a critical follow-up. General liability is what protects your property from damage, but workers' comp is what protects you if one of their employees gets hurt on your property. You need them to have both, period."What are your policy limits?"

You're looking for a general liability policy of at least $1,000,000. That number might seem high, but it ensures there's enough coverage for a major accident, protecting your single biggest asset: your home."What kind of bond do you have?"

For any service that brings workers into your home, like window cleaning, you want to hear that they carry a janitorial bond or a business service bond. This is the specific type of bond that protects you from employee theft.

If a contractor gets defensive or hesitant about sending you their Certificate of Insurance, walk away. It's that simple. Reputable companies expect this request and have the paperwork ready to go. It’s a standard part of doing business responsibly.

Interpreting the Answers and Spotting Red Flags

Asking the questions is step one, but you also need to listen carefully to the answers. A vague response or a defensive attitude can be just as telling as a flat-out "no."

A true professional will respect your diligence. They'll see it as a sign that you're a serious homeowner, which makes for a better working relationship. On the flip side, a company that cuts corners will often get evasive or try to downplay the importance of these protections. That's your cue to find someone else who takes your family's security seriously.

Green Flags (What you want to hear):

- "Absolutely, I can email you our Certificate of Insurance this afternoon."

- "Yes, we are fully insured with a $2 million general liability policy and carry full workers' compensation for all our staff. We also have a janitorial bond to protect our clients."

- "That's a great question. Our bond covers employee theft up to $25,000."

Red Flags (Warning signs to watch for):

- "Don't worry, we're very careful. We don't need insurance."

- "Yes, we're insured." (But they can't or won't provide the COI).

- "My bond covers any problems on the job." (This is misleading; a bond doesn't cover property damage or accidents).

By asking these direct questions, you can feel confident that any company you hire, including those for residential window cleaning services near you, has the right protections in place. It's a simple step that delivers priceless peace of mind.

Why This All Matters for Your Peace of Mind

It’s one thing to understand the difference between "bonded" and "insured." It’s another thing entirely to hire a company that lives and breathes client protection. At Sparkle Tech Window Washing, our goal isn't just to leave you with sparkling, streak-free windows—it's to give you complete peace of mind from the moment our truck pulls up.

That's why we don't just have insurance and bonding; we consider them a non-negotiable part of our promise to you. Our extensive general liability and workers' compensation policies are always in place to make sure a simple, unforeseen accident never turns into your financial headache.

We're More Than a Service; We're a Partner You Can Trust

Let's be honest—when you invite a service team into your Scottsdale or Peoria home, you're placing a huge amount of trust in them. We get that, and we honor it by taking every possible step to protect you, your family, and your property. Being fully bonded and insured isn't just a selling point for us; it’s tangible proof of our commitment to professionalism.

Think of it this way: our service guarantee ensures you'll love the results. Our insurance and bonding protect you from the "what-ifs." Together, they create a safety net so you can have total confidence in our team, knowing we're prepared for absolutely anything.

For us, proper coverage is a core value. It’s a direct reflection of our promise of reliability, showing that we stand behind our work and are fully accountable for our presence on your property.

Choosing a company that invests in this level of protection says a lot. It shows they respect their clients enough to put safeguards in place before they're needed. It proves they're a stable, professional outfit built for the long haul, not just a crew looking to make a quick buck. This is the standard we bring to every home we service, from Phoenix to Anthem.

Your Assurance of a Worry-Free Experience

Ultimately, the reason this coverage matters so much is simple: it lets you relax. You don't have to stand there worrying about the "what-ifs." What if a ladder slips and damages a window frame? What if an employee is dishonest? When you hire a fully protected company like Sparkle Tech, those concerns are already taken care of.

Our team is trained to work with extreme care, but we're also realists. Accidents, though rare, can happen in any line of work. Our insurance is our plan to manage that risk so it never, ever falls on you. This frees us up to focus on what we do best—making your windows shine—while you get to enjoy the beautiful results without an ounce of stress.

For our neighbors in the communities we serve, choosing us means you're picking a partner who has already thought through every detail of your protection. If you're looking for a team that values your security as much as you do, learn more about our commitment to providing affordable window cleaning near you. Your home is your biggest investment, and it deserves nothing less than the highest standard of care and protection.

Got Questions? We’ve Got Answers.

It’s completely normal to still have a few questions, even after getting the lowdown on bonding and insurance. Let's tackle some of the most common ones we hear from homeowners.

Is a Business License the Same as Being Bonded and Insured?

Great question, but no—they are three totally different things, and you want a contractor who has all of them.

Think of it like this: a license is just permission from the state or city to open up shop. It means they've met the bare-minimum legal requirements to do business. On the other hand, being insured and bonded are all about protecting you. Insurance handles accidents, and a bond protects you from theft or shady work. A pro will have all three, no exceptions.

What Happens if an Uninsured Worker Damages My Property?

Honestly, it’s a nightmare scenario. If a contractor without general liability insurance puts a ladder through your brand-new picture window, your only real option is to take them to court.

That means hiring a lawyer and heading to civil court, a process that can drag on for months and cost a fortune in legal fees. Even if you win, there's no guarantee the contractor has the money to pay you back. This is precisely why you must see proof of insurance before anyone sets foot on your property. It's your financial safety net.

Your own homeowner's policy might cover the damage, but that's a risky path. Filing a claim against your own insurance for a contractor's mistake will almost certainly cause your premiums to spike. The contractor's policy should always be the one to pay.

Will My Homeowners Insurance Cover Accidents Caused by a Contractor?

Your policy is really meant to be a last resort, not the first line of defense. Relying on it to cover a professional's mess can jack up your rates for years or even get your policy canceled.

A contractor's general liability insurance is specifically designed to cover the risks that come with their job. Make sure they use it.

For a team that takes your protection seriously, trust Sparkle Tech Window Washing LLC. We are fully licensed, bonded, and insured for your complete peace of mind. Schedule your service today!